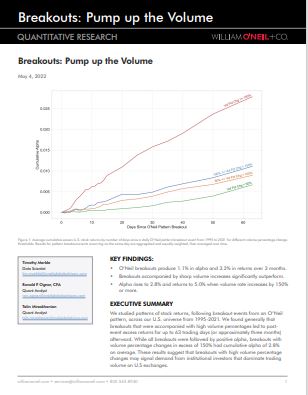

Breakouts: Pump Up the Volume

We studied patterns of stock returns, following breakout events from an O’Neil pattern, across our U.S. universe from 1995‒2021. We found generally that breakouts that were accompanied with high volume percentages led to post-event excess returns for up to 63 trading days (or approximately three months) afterward. While all breakouts were followed by positive alpha, breakouts with volume percentage changes in excess of 150% had cumulative alpha of 2.8% on average. These results suggest that breakouts with high volume percentage changes may signal demand from institutional investors that dominate trading volume on U.S exchanges.